I love you, but I don't! Our complicated relationship with taxes

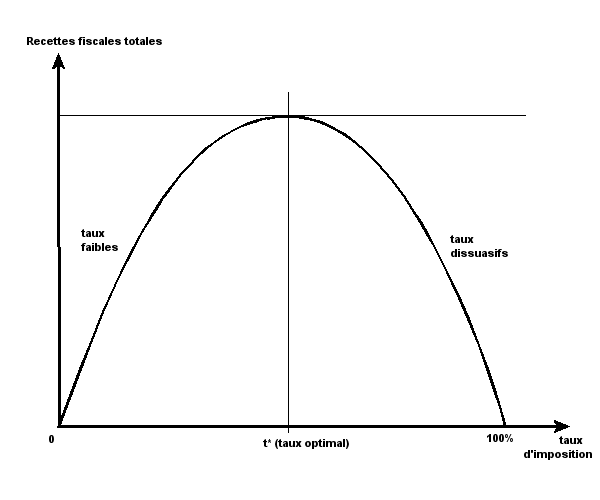

“Too much tax kills tax,” as the famous saying by American economist Arthur Laffer goes. But what if, in France, it were more complicated than that? Aren’t there other social, emotional, or moral considerations to take into account?

Cecile Bazart, University of Montpellier; Aurélie Bonein and Thierry Blayac, University of Montpellier

At a time of recurring government deficits, many of the solutions discussed in public debate focus on combating tax evasion. Media coverage of this standoff between wealthy taxpayers and the tax authorities often employs combative language that emphasizes the detection and punishment of tax evaders for the common good.

The bill introduced in November 2025 is in line with this approach and has a threefold stated objective: “better prevention and detection, better enforcement and penalties, and better recovery.” The political discourse aimed at restoring the legitimacy of taxation is based on the need to crack down on behavior deemed criminal.

While taxation has historically been the financial tool used to raise the resources necessary for the functioning of the state, it is nonetheless a complex social phenomenon. This is what our research highlighted. For, in addition to financial gain, numerous other social, emotional, and moral considerations explain our complex relationship with taxation.

{kind=link}

Only 14% of taxpayers pay their taxes out of fear of an audit

It is clear that enforcement alone does not deter fraud. Other factors influence the decision to pay or to commit fraud.

In our 2015 survey, conducted with Thierry Blayac among 1,094 taxpayers, we showed that the primary motivation for paying taxes is a sense of civic duty. This was the response given by 45% of respondents; 25% cited the provision of public goods and services as their motivation for paying taxes; and approximately 10% paid for more general moral reasons. Ultimately, only 14% of those surveyed said they paid taxes out of fear of a tax audit and its consequences.

These findings on the diversity of motivations for paying taxes broaden the discussion on tax acceptance. They suggest that providing greater transparency about what taxes fund improves public perception of the tax system. In fact, 11% of taxpayers surveyed cited a lack of transparency regarding the use of tax funds as a reason for opposing taxation. Taxes will be viewed more as an exchange than as a levy.

Our study also highlights that complexity hinders a proper understanding of the tax system and increases tax evasion. For 21% of the taxpayers interviewed, the complexity of tax legislation is a problem, while 13.5% believe that reforms occur too frequently and 10.5% feel that administrative procedures are too complex.

French Tax System Deemed Unfair

Taxation is a social phenomenon. It is based on a vision of the relationships between individuals and of solidarity within society. It creates a bond among taxpayers, since tax evasion by some results in additional costs for others. This interdependence among citizens lies at the root of a divide between those who pay their taxes and those who evade them. It fuels the perception of tax injustice, which has a powerful impact. Our study highlights that the French tax system is generally perceived as unfair, with a score of 4.11 out of 10.

In a series of experimental studies, Aurélie Bonein and I demonstrated that social comparison can lead to an increase in fraud. Information about others’ offenses leads to an increase in fraud among others. More specifically, in this research, we tested two types of tax injustice:

- Related to a tax rate differential arising from the application of different tax rates to individuals who are tax-identical, without further justification.

- Related to tax evasion—some people evade taxes, while others do not.

We demonstrate that while both types of injustice fuel tax evasion, the effect of social comparison is stronger than that of injustice related to tax rates. It is conceivable that this tax reciprocity could be leveraged to create a social dynamic that encourages honesty, particularly if a signal is sent that tax evasion leads to social disapproval.

Lack of Tax Knowledge

Since taxation is a social phenomenon, it is also heavily influenced by a country’s fiscal history and by people’s understanding and perceptions of taxes. In the survey described above, we also assessed our respondents’ understanding of the tax system.

It appears that taxpayers’ perceptions are out of step with their knowledge—estimated at 33.44% based on a few basic questions. This very low level of understanding of taxation does not support a well-founded perception of injustice. On the contrary, this bias leaves ample room for subjectivity and emotion. It raises questions about the underlying causes of the current loss of legitimacy of taxation.

Ultimately, is tax evasion a genuine challenge to the tax system, or is it the result of misunderstandings and emotions stemming from tax fatigue?

Cecile Bazart, Associate Professor, Montpellier Center for Environmental Economics (CEE-M), University of Montpellier; Aurélie Bonein, Associate Professor of Economics, Center for Research Economics and Management (CREM); and Thierry Blayac, Professor of Economics, Montpellier Center for Environmental Economics (CEE-M), University of Montpellier

This article is republished from The Conversation under a Creative Commons license. Readthe original article.