Music in the Crosshairs of Industrial Conglomerates

The French music industry is being shaken up by the unprecedented entry of corporate groups across its entire scope of operations. This trend began in 2004 with the emergence of Live Nation and the launch of its first festival: Main Square, in Arras.

Emmanuel Négrier, University of Montpellier

Since then, the music industry—which had previously been based on a mixed-economy model and a multitude of small businesses (subsidized festivals, producers representing a small number of artists, and municipal or mixed-economy venues)—has been the scene of a wave of acquisitions by a handful of operators.

Trends toward diversification and concentration are evident. Diversification is characterized by the entry of companies that were once specialized in a single segment (production, venue management, festival management, record labels, etc.) into other segments. These companies may be primarily French, such as Fimalac, Vente-privée, Morgane, and LNEI; or multinationals such as Vivendi, AEG, or Live Nation. Concentration manifests itself in the takeover, by a limited number of companies, of firms that were once interdependent but operated in subsectors governed by their own expertise and rules. Mergers therefore pose the challenge of integrating not only business lines but also legal statuses that were previously separate.

This concentration is “diagonal” because it draws on the three types of concentration traditionally distinguished in industrial economics—and particularly in the media sector (financial, horizontal, and vertical). The reasons behind it are varied, and not all of them are driven by profitability. Perhaps this is what makes it enigmatic and fragile.

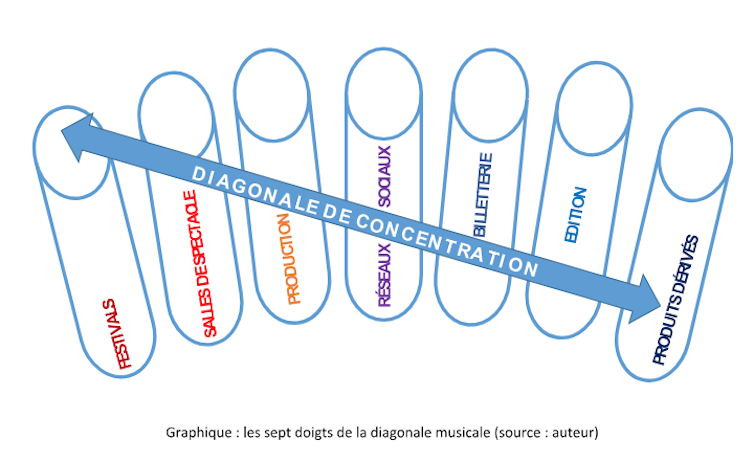

A " diagonal " concentration

The first type of consolidation is financial and allows one company to take control of another while allowing it to retain formal autonomy and its brand identity. Fimalac, led by Marc Ladreit de Lacharrière, is a good example of this model, with revenue of nearly 250 million euros (in 2016) generated by its entertainment division (3S Entertainment), which, as of late 2016, comprised 101 performance venues and 12 production companies, some of which, such as Miala, organize festivals. The goal of preserving brand identities is to avoid a sudden break with the personalized approach that contributes to the value of these companies, which are often small-scale and fragile. This does not preclude economies of scale, such as the consolidation of ticketing operations, for example.

In this first type of consolidation, we find players that specialize in several niches at once without, however, encompassing the entire artistic value chain. Fimalac’s strategy specifically aims to avoid a “360-degree” approach in the name of artistic diversity, whereas Vivendi (nearly 11 billion euros in 2016) intends to cover everything from development to production and artist tours, all the way to promoting artists in the media and the recording industry, using the group’s full range of resources.

The second form of concentration is horizontal and takes the form of the acquisition of competitors or the duplication—within the same subsector—of an event, for example. Examples include the Live Nation group and its variations of the same festival in several countries—such as Lollapalooza—as well as the approximately 3,300 artists under contract who tour worldwide, particularly during the 25,500 concerts organized annually by a group whose revenue stood at 7.5 billion euros in 2016. This phenomenon is not as recent as it seems, since in the classical music sector, René Martin had—albeit on a more modest scale (and without the same capital implications as owning a production company or festivals)— replicated his festival La Folle Journée in several major cities, while also taking the helm of other festivals in France (Saint-Chartier, La Roque-d’Anthéron).

We can also mention the Lagardère Group and its strategy for managing artists, just as the company had previously pioneered the management of top athletes’ careers. This focus on a single business niche creates expectations of economies of scale on a larger scale than in the previous case. For example, replicating an event allows for the pooling of certain costs: graphic design, bulk artist fees, consistency in technical setup, communications, etc.

The third form of concentration is vertical and involves the acquisition of customers or suppliers. This approach moves closer to a “360-degree” model —more or less completely—by capitalizing on the interdependencies between the initial risks (in developing an artist, creating a label, establishing a cultural venue, etc.) and the profits derived from all possible forms of exploitation of an artist or a work. We see this in the cases of Fimalac, Vivendi, and Live Nation, already mentioned. We can also mention Sony, in the areas of equipment and recorded music, whose investment in artist production is, of course, linked to the collapse of profitability in recorded music and the shift of profit sources toward live performances.

Diagonal consolidation is closely linked to the fact that it is impossible to categorize operators into a single niche. It is by examining each of these areas—venue management, festival organization, production, publishing, digital services, ticketing, merchandise, etc.—that we can observe the ongoing interpenetration of these sectors. But how can we explain this sudden industrial passion for music? There is a paradox here that warrants further examination: most of the strategies implemented by these groups in France—such as the acquisition of festivals, venues, and record labels—are currently resulting in losses. This is strange for captains of industry who, incidentally, maintain a level of business secrecy that contrasts sharply with the very public nature of their investments. Let’s try to shed some light on their motives.

What drives these concentration trends?

There are five reasons behind these major maneuvers: passion, mediation, vision, attention, and support.

Passion evokes these leaders’ emotional connection to music. On the enchanting side, it’s the prince’s classic delight in seeing himself reflected in the artist he patronizes. From a strategic perspective, culture serves to symbolically elevate one’s status, especially when one’s business success has been built on shady stock market dealings or dubious sex trade operations, as Laurent Mauduit pointed out regarding the media in his 2016 book *Main Basse sur l’Information*.

Mediation involves leveraging a prominent position in the music industry to foster other, more profitable ventures. Financial losses in the music business are offset by the fact that in VIP lounges and during conversations with elected officials on the sidelines of a festival, contracts are signed, support is secured, and deals are negotiated in the excitement of the moment. Losing (a little) leads to winning (big). All while donning the mantle of a hero, savior of French culture, and benefactor of the arts. On April 22, 2017, he told *Le Monde* that his strategy makes his group “the secular arm of the Ministry of Culture” (*Le Monde*, April 22, 2017, interview by Fabienne Darge and Philippe Dagen).

These leaders’ vision is rooted in their anticipation of the sector’s deregulation, which is in line with current trends: the reduction of public subsidies, which, in their view, distorts competition; and the implementation of trade agreements, such as CETA, which exclude the music sector from the scope of the cultural exception. Today, we are losing in order to gain more tomorrow. And in fact, we are losing very little, since we are buying festivals and venues at prices that take no account of the subsidies paid out over the years. For example, AEG’s acquisition of the Rock en Seine festival took place without any consideration of the significant subsidies granted to the event for years by the Île-de-France Regional Council. Yet it is fair to say that these subsidies played a major role in establishing the event’s value, without providing the local community with any financial return whatsoever upon a buyout.

This trend is linked to a new economy driven by the ability to use information related to users’ behavior on social media or during their online interactions. By entering this sector, industrial groups gain access to metadata collected during ticket purchases and interactions on forums and social media platforms. It is no coincidence that these groups are investing in ticketing services: Ticketmaster (Live Nation), Vivendi Ticketing, My Ticket, and Tick&Live (Fimalac). This is where the sources of profit (and standardization of offerings) lie, linked to the “attention economy” discussed by Yves Citton. The personality profile derived from a ticket purchase can take commercial exploitation a long way, starting from an initial act—buying a show ticket—that carries an extremely positive emotional charge. The perfect algorithm!

A safety net for tough times

As for the financial aspect, it reduces the burden to a purely material level. But it is true that even if a little money is lost, assets have nonetheless been acquired—in the form of theaters, publishing houses, broadcasters, etc.—which represent tangible assets, particularly real estate, and strengthen these companies’ equity in a relatively uncertain environment. Thus, in the event of a bubble bursting, this serves as a safeguard against a severe downturn.

![]() Once these motivations have been explained, doubts remain about their cultural value in France or elsewhere. Naturally, these groups believe they contribute in their own way to artistic creativity, given the breadth of their artist rosters. But their growing influence over programming and their control over the most attractive lineups underscore the risk these strategies pose in terms of diversity, and artists' increased dependence on these firms. This could be the subject of a separate discussion, which would also examine ways to counteract its most harmful effects: the standardization of events, rising prices linked to increases in artists’ fees and safety standards, and the reduction of artistic risk due to the concentration of lineups around “ house ".

Once these motivations have been explained, doubts remain about their cultural value in France or elsewhere. Naturally, these groups believe they contribute in their own way to artistic creativity, given the breadth of their artist rosters. But their growing influence over programming and their control over the most attractive lineups underscore the risk these strategies pose in terms of diversity, and artists' increased dependence on these firms. This could be the subject of a separate discussion, which would also examine ways to counteract its most harmful effects: the standardization of events, rising prices linked to increases in artists’ fees and safety standards, and the reduction of artistic risk due to the concentration of lineups around “ house ".

Emmanuel Négrier, CNRS Research Director in Political Science at CEPEL, University of Montpellier, University of Montpellier

The original version of this article was published on The Conversation.