Oil prices over $80: bad for the economy, good for the climate?

When he left the government, Nicolas Hulot cited the rise in greenhouse gas emissions in 2017 as one of the reasons for his resignation. This increase, which is highly damaging to the climate, was primarily the result of the drop in oil prices between 2014 and 2017; which boosted economic activity and encouraged greater consumption of petroleum products, as they became more affordable for consumers.

Christian de Perthuis, Paris Dauphine University – PSL and Boris Solier, University of Montpellier

Shutterstock

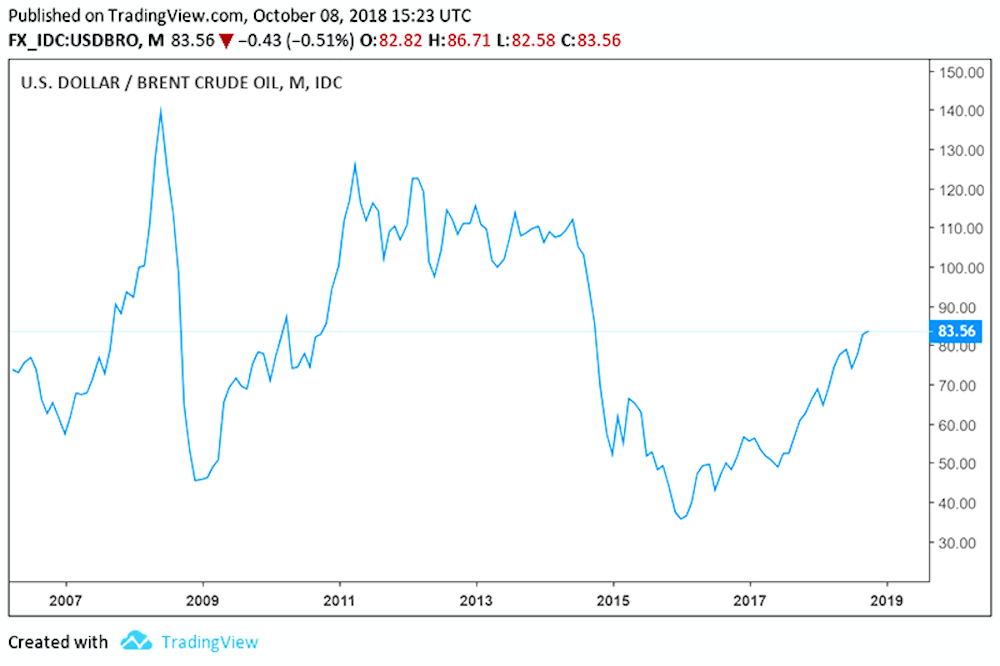

A turnaround in 2018: At over $80 a barrel, the price of Brent crude reached its highest level in four years in early October (see the figure below).

Bad news for the economy, but a positive incentive for the climate? Let’s take a closer look.

tradingview.com

Why high oil prices are weighing on the economy

Rising oil prices erode household purchasing power in much the same way as a carbon tax without a mechanism to redistribute revenue to low-income households, and they drive up production costs for energy-intensive industries.

According to the Mésange macroeconometric model, used by the Ministry of the Economy, a 20% increase in the price per barrel leads to a 0.2 percentage point reduction in GDP after two years. The doubling of crude oil prices over the past year and a half could therefore cost one percentage point of growth. Economic forecasters, take note!

One might wonder whether this short-term view is not overly simplistic. The rise in oil prices is likely to result merely in a transfer of value between producers and consumers, and thus lead to a geographical shift in value added rather than a decline in economic activity.

This reasoning holds true if we consider only the flow of goods. However, we must also take debt levels into account. In Western economies marked by decades of debt, the burden of private debt constitutes a major vulnerability in the system. We saw this, for example, during the 2008 crisis, when oil prices exceeding $140 per barrel contributed to an increasing number of American households becoming unable to repay their mortgages and precipitated the collapse of the American investment bank Lehman Brothers.

It is therefore necessary to take into account the effect of rising oil prices on the debt burden—which structurally weakens economies—in order to accurately anticipate their economic impact.

High oil prices aren't so good for the climate

From the demand side, higher oil prices encourage people to be more careful about their purchases of gasoline, heating oil, and natural gas, whose prices are increasingly linked to that of oil. This hurts consumers but is good for the climate. For an environmental activist, between losing a percentage point of growth and saving the planet, there’s no contest.

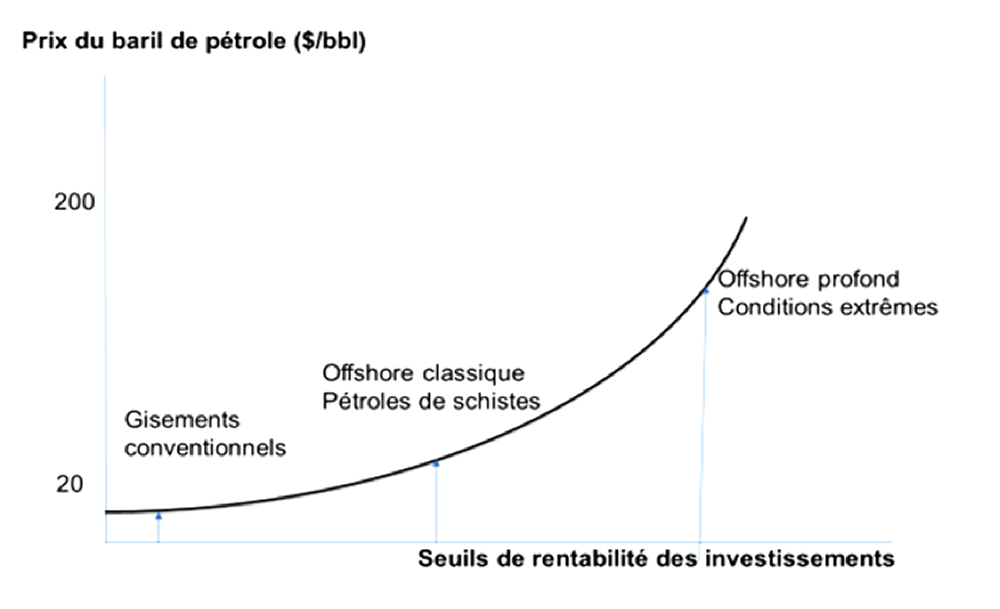

But at the same time, rising oil prices send another signal to producers. As the price per barrel rises, it becomes increasingly profitable to extract oil from less accessible—and therefore much more expensive—reservoirs: thousands of meters below the sea, in the Arctic, or in oil shale. With every oil price boom, we see a resurgence in exploration and production investments that will drive tomorrow’sCO2 emissions.

This is the dark side of the oil rent economy for the climate. It has two sides: scarcity rent and differential rent.

When the relative scarcity of oil increases—whether for geological or geopolitical reasons—the price per barrel skyrockets. It can exceed $100 per barrel, as it did in 2008 or 2011–2014. The rising price of oil increases the scarcity rent captured by producers, which encourages them to invest in new capacity and unconventional extraction technologies… and thus to increase the potential forCO2 emissions in the medium and long term (see the figure below).

The excess supply eventually catches up with demand—which has been slowed by rising prices—and causes prices to fall. This is the cyclical phenomenon of “oil counter-shocks.” This decline stimulates demand and fuels a resurgence inCO2 emissions. This is bad news for the climate in the short term, especially since producers are showing unexpected resilience to falling prices. This is where the second aspect of oil rent comes fully into play: differential rent.

The vast majority of producers pocket a second windfall resulting from the difference between their operating costs and those of fields that are less favorably located or produce lower-quality crude. When the price per barrel drops to $20, the least well-positioned producers suffer. But the Ghawar field in Saudi Arabia remains highly profitable: its production cost is around $5 to $7 per barrel. Its operator is not about to exit the market.

It feels like we’ll never get out of this! Yet there is a tool that can help us break this cycle: carbon pricing, which provides incentives for climate action on both the producer and consumer sides. A recent publication by the “Climate Economics” Chair explores this aspect in depth, focusing on the energy transition and the ticking of the climate clock.

Carbon rent versus oil rent

The cornerstone of the carbon rent economy is the value placed on climate protection through acarbon price. This price is a cost that must be applied to all anthropogenicCO2 emissions. It does not matter whether it is introduced into the economy via a tax, a permit market, or more implicitly through a set of standards. Its distinctive feature is that it provides the right incentives on both the supply and demand sides.

From the consumers’ perspective, the introduction ofa carbon price leads to higher costs for different energy sources in proportion to their respectivecarbon content. The incentives created are twofold: first, to conserve energy whose average cost is rising; and second, to replacehigh-carbon energy sources with low-carbon or carbon-free alternatives.

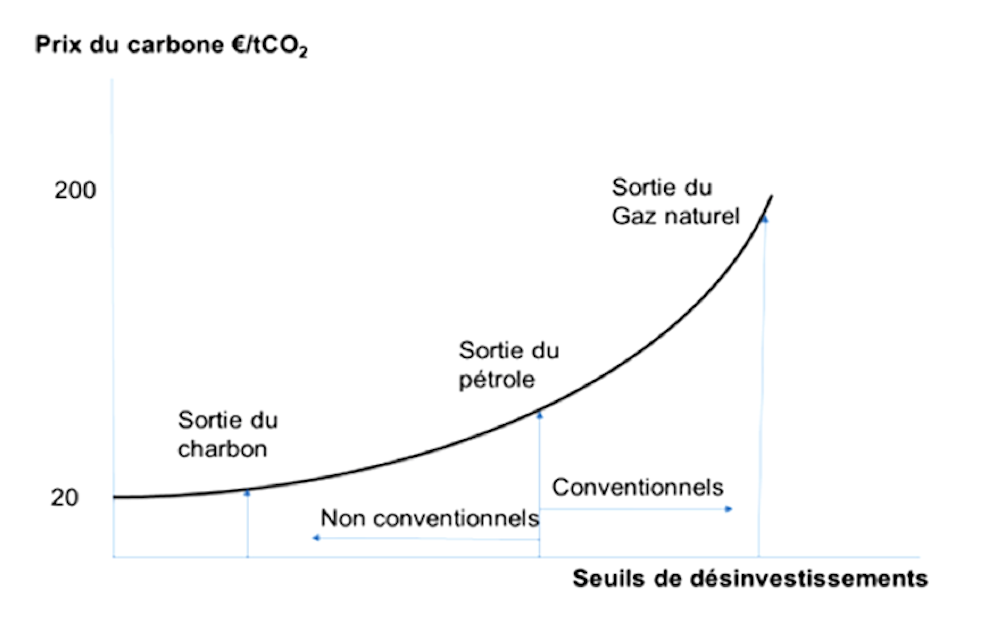

In a carbon rent economy, positive incentives for consumers are no longer offset by a countervailing effect on the part of producers, who are incentivized by rising prices to expand their fossil fuel production capacity. As soon as the price of carbon becomes the guiding principle of the energy transition, it becomes less and less profitable to invest in fossil fuels as the cost ofCO2 rises (see the figure below). The rising cost ofCO2 diverts both producers and consumers away fromCO2-emitting fossil fuels.

As long as the carbon rent economy has not supplanted the oil rent economy, there will be a contradiction between how markets function and the goal of reducing CO₂ emissions2. Consequently, there is a contradiction between the goals set by the Secretary of the Environment and the traditional indicators of employment, purchasing power, and growth that guide government action.![]()

Christian de Perthuis, Professor of Economics and founder of the Chair in Climate Economics, Paris Dauphine University – PSL and Boris Solier, Associate Professor of Economics, Research Associate at the Chair in Climate Economics (Paris-Dauphine), University of Montpellier

The original version of this article was published on The Conversation.