The profound uncertainty of the global financial system

Every year, the traditional summer lull is accompanied by comments—some more insightful than others—from economic analysts on duty regarding the situation expected when business resumes in September and the economic outlook for the final quarter of the year.

Roland Pérez, University of Montpellier

For this annual exercise—which can sometimes feel like a tired old ritual—analysts scrutinize subtle signals that might provide clues to support their predictions. In 2019, however, they won’t need to go to such lengths to gather meaningful details, as the events, facts, and observable information from recent weeks are so numerous and sufficiently consistent that they allow for a well-documented analysis.

Most of these are linked to the steady stream of tweets from U.S. President Donald Trump, who, week after week, attacks anything he perceives as hindering his “America First” slogan; After Iran, Mexico, Venezuela, the European Union, and so many other countries, he is now once again targeting China, a country with which he wishes to reduce the structural trade deficit through the traditional means of import tariffs. But China is not Venezuela, and it has begun to fight back, on the one hand by reducing some of its imports from the United States, and on the other by allowing its currency to depreciate on the foreign exchange markets.

These two developments are cause for concern, as they signal the onset of a trade war, waged through the traditional tools of tariffs and exchange rates. While we know how such a conflict begins, no one can predict either its scale or its outcome. Given that this is a confrontation between the two giants of the global economy, a lose-lose outcome for both parties cannot be ruled out, with significant collateral damage for the rest of the world.

Pre-election atmosphere in the United States

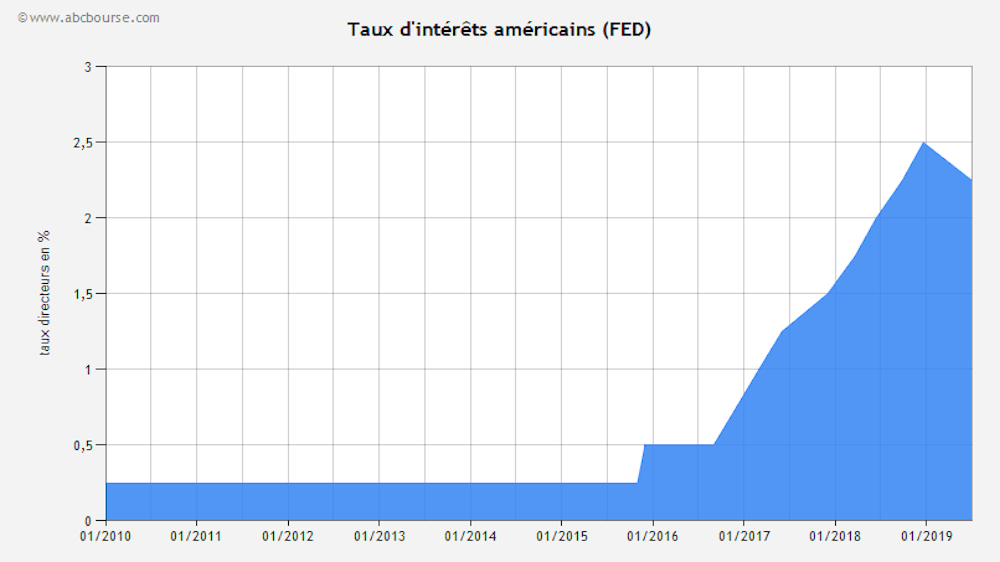

It is within this same context that we must view monetary policy developments as reflected in the actions of central banks. Over the past dozen years—primarily in response to the 2008 global financial crisis —these central banks (Japan, followed by the United States and the EU) have implemented so-called “accommodative” monetary policies, resulting in a sustained decline in key interest rates—approaching zero or even negative levels—and virtually unlimited purchases of bank debt (“quantitative easing”).

The strong performance of the U.S. economy in recent years had allowed Federal Reserve (Fed) officials to begin returning to a more conventional policy stance, which resulted in a gradual increase in key interest rates. That was before President Trump stepped in, calling for another cut in those rates.

This internal conflict has so far resulted in a slight cut (a quarter of a point) in the key interest rate—a concession by the current Fed chair—accompanied, moreover, by a solemn warning from four former chairs expressing their concern about the central bank’s independence from political influence. No one can, at this point, predict how the various positions will play out in practice in the coming months, especially given the pre-election climate the country has entered.

The financial markets, which abhor this kind of uncertainty, have begun to panic. In just a few trading sessions in August, the major indices lost a substantial portion of the gains they had made since the start of this year. Given that this rally has itself been part of a virtually uninterrupted uptrend since the 2008 financial crisis, the real question analysts are asking is whether these recent jitters signal the start of a lasting reversal of the financial markets’ bull cycle or a blip linked to current uncertainties regarding public policy.

Abundant cash reserves

To attempt to answer this question without preconceptions, we need to examine the current situation of companies listed on these markets. Several observations stand out:

- First of all, most of these large publicly traded companies have benefited greatly from accommodative monetary policies, which have provided them with virtually unrestricted financing (bank loans or bonds) at very low cost, thereby reducing their average cost of capital and altering their financing structures.

- Nevertheless, the capital expenditures made in recent years by the major firms in question have not been exceptional, falling within the average range of previous years. As a result, many companies and corporate groups have ample cash reserves awaiting investment.

- Conversely, there has been a significant increase in share buybacks by publicly traded companies themselves, particularly in the United States, where such transactions are subject to less regulation than in the past; this has resulted in support for stock prices and an increase in leverage, or even double leverage when these buybacks have been financed through additional debt.

- These financing facilities, combined with the generous tax breaks provided in particular by the current U.S. administration, have led to excellent net results, further boosting stock prices.

- These various factors combine and can result in the profile of a large publicly traded company with strong financial and stock market performance, and a balance sheet that includes both an abundance of cash on the asset side and significant debt on the liability side.

This situation—one with which many companies around the world would be content—raises concerns for us regarding its significance, intrinsic quality, and sustainability. Accounting performance, and even more so stock market performance, is not directly linked to the business model being followed, but rather to the financial transactions carried out (such as debt issuance and share buybacks); there is no guarantee that these favorable effects will persist in the future unless their continuation is engineered through monetary policies (regarding the cost of debt) or stock manipulation (regarding share buybacks).

Warning signs of a recession

This brief analysis—which would obviously need to be refined by company type and industry— leads us—if we are to offer our own assessment—to conclude that the U.S. economy and its financial markets are indeed at the end of a bull market cycle that began with the rescue measures implemented after the 2007–2008 crisis to address that major crisis.

Signs that can be interpreted as early indicators of a turnaround in the global economic climate and its impact on the markets have emerged in a consistent manner:

- On the economic front, while indicators of U.S. economic activity remain positive, concerns are emerging regarding the consequences of the trade war with China. These concerns led President Trump, in a typical about-face, to postpone for several months the new tariff measures he had announced, notably to protect consumers worried about price hikes during the Christmas season… Elsewhere in the world, the economic situation is more concerning, with indicators already deteriorating (Germany) or on the verge of doing so (United Kingdom).

- In terms of interest rates, we have seen a “yield curve inversion” between short-term and long-term U.S. Treasury bonds, a sign that analysts interpret as a harbinger of a recession.

- In the stock markets, on several occasions in the major U.S. financial centers, it was the companies themselves—through their share buybacks—that acted as the counterparties to other categories of market participants (individuals, investment funds) who were “net sellers.”

Investment funds appear to be aware of this concerning situation, and many of them are adopting a wait-and-see approach, much like Warren Buffett’s iconic fund, which has more than $120 billion in cash waiting to be invested.

These various factors interact; some of them—such as the wait-and-see attitude of investment funds—are both a consequence of the other factors identified and a contributing factor to the problem.

The G7 with its back against the wall

The leaders of institutions responsible for economic and financial policy are aware of this risk of a reversal, but have little room to maneuver. Central banks are mired in their policies of quantitative and interest rate easing, which, as consultant Jacques Ninet put it in his 2017 essay, is something of a “black hole of financial capitalism.” President Trump is also aware of this, but will do everything in his power to ensure that a new financial crisis does not erupt before the next political deadlines or, if such a crisis were to occur, to shift the blame onto others (the Fed, China, etc.) and absolve himself of responsibility.

The upcoming G7 summit, scheduled for August 24–26 in Biarritz, will inevitably feature a likely “heated” exchange among these leaders. French President Emmanuel Macron, who will host the summit on behalf of France, will certainly attempt to outline a solution that offers the parties involved at least a minimally acceptable outcome. He should be able to count on some G7 members and on the new leaders appointed, with his support, to head the European Central Bank (ECB) and the International Monetary Fund (IMF). This is no sure thing, because in the financial sector more than any other, mutual trust among the leaders responsible for implementing a program of action is essential to the success of those actions.![]()

Roland Pérez, Professor Emeritus, Montpellier Research in Management, University of Montpellier

This article is republished from The Conversation under a Creative Commons license. Readthe original article.