Share Buybacks: In the Face of Market Excesses, Regulation Remains Too Timid

Current events in today’s world are full of major issues on which the public expects economic and political leaders to take concrete actions that can help improve the situation. Among these many current issues, we wish to focus on a company’s buyback of its own shares—transactions that appear technical and are little known to the public. Yet these transactions deserve to be examined for the behaviors they reveal and their economic impact.

Elisabeth Walliser, Université Côte d’Azur and Roland Pérez, University of Montpellier

Over the years, these transactions—which were once rare or even prohibited—have become very common. These share buybacks significantly alter the functioning of financial markets, as they can be seen as a form of stock price manipulation.

Back in 2019, we had already drawn attention to this worrying trend in the U.S. stock markets. Since then, this trend has persisted, driven by “accommodative” monetary policies ” (quantitative easing, or QE, in Europe, and zero interest rate policy, or ZIRP, in the United States) that facilitate access to credit and amplified, in the United States, by the tax measures enacted under President Donald Trump to encourage American multinational corporations to repatriate liquid assets held abroad.

Yardeni.com

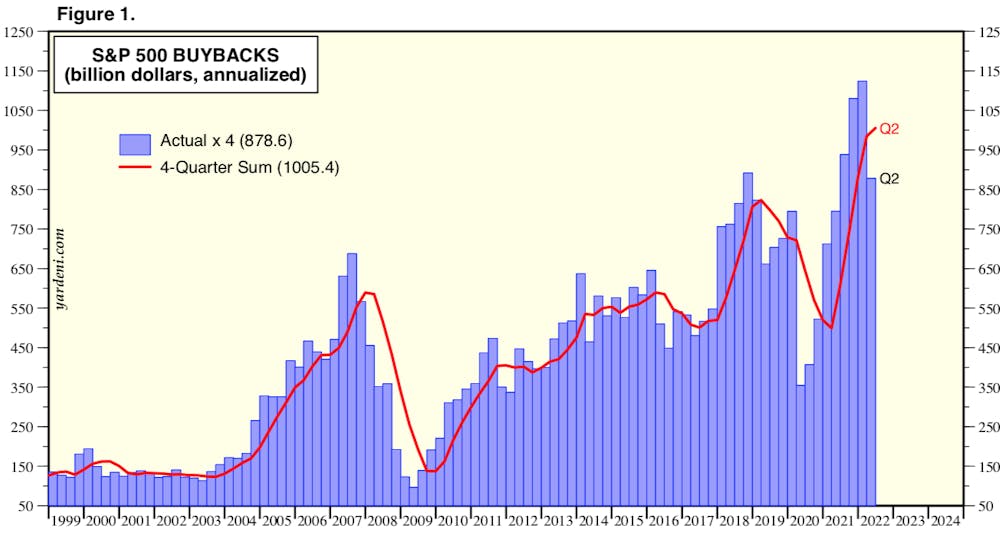

By the end of 2021, the total value of these share buybacks had even surpassed the $1 trillion mark in annual flows for the S&P 500 alone—the stock index comprising 500 major publicly traded companies. These annual flows have now exceeded the amount of dividends paid out. For example, in 2021, Apple conducted $85.5 billion in share buybacks compared to $14.5 billion in dividends. Over the past ten years, the total amount of share buybacks by the Cupertino-based company has reached $567 billion. In some years, the total cash flow from dividends and share buybacks even exceeded the cash flow from new share issuances, thereby reversing the financing function of financial markets.

A trend that is gaining ground in Europe

In other parts of the world, these transactions are less massive but are beginning to gain significance. On September1, the newspaper Les Échos reported: “Major European companies have turned en masse to share buybacks since the pandemic. These buybacks have tripled in one year, reaching 70 billion euros in the first half of the year in Europe, including 15 billion in France.”

“As such, the TotalEnergies group has launched a new share buyback program ‘in line with its announced policy of allocating up to 40% of the excess cash generated above $60 per barrel to share buybacks,’ the same newspaper noted a month earlier; these buybacks are expected to reach $7 billion in 2022.”

[Nearly 80,000 readers rely on The Conversation’s newsletter to better understand the world’s major issues. Subscribe today]

Given the scale of this near-tsunami, it is surprising how muted the reactions have been, both from the relevant authorities and the research community. As for the authorities responsible for these issues, the measures taken or being considered are modest. In the United States, after much hesitation, the Securities and Exchange Commission (SEC), the U.S. securities regulator, issued new regulations governing these transactions in late 2021, aimed primarily at improving the required disclosure. Additionally, the U.S. Senate passed a bill in August 2022 imposing a small tax (1%, effective as of January 2023).

In other parts of the world, however—particularly in Europe—we have not yet heard of any proposed decisions on this matter, unlike on other related but distinct issues, such as “superprofits” and their potential taxation…

Mainstream finance

The silence—or at least the scarcity—of research devoted to the issue of share buybacks seems all the more surprising. Admittedly, there are a number of studies that have focused on these issues, sometimes with great insight; but the researchers involved are often marginalized in the academic world of finance. The latter remains largely dominated by a theoretical framework developed over several decades, forming a paradigm—known as “mainstream finance”—from which researchers, it must be acknowledged, find it difficult to break free.

Thus, a share buyback can be easily explained using the concept of free cash flow, which refers to the cash flow available once investments have been recouped. Executives are encouraged to return this excess cash to shareholders rather than use it in a suboptimal manner. A share buyback thus appears as a means of disciplining management and reflectsshareholder-oriented corporate governance, as recommended by this school of thought.

Such a theoretical justification may have raised a few eyebrows among many finance professionals. Admittedly, share buybacks can be the appropriate solution for resolving specific situations (for example, the death of a co-founder of a company whose remaining partners wish to retain exclusive control) or, more broadly, for publicly traded companies, to modify the ownership structure by reducing the free float in favor of long-term shareholders.

Nevertheless, beyond these capital restructuring initiatives, the primary purpose of these share buyback announcements is to please shareholders in the short term by propping up the stock prices of the companies involved. Executives who propose such maneuvers also stand to benefit, as strong stock prices have become a key indicator of their ability to “create value,” and incentive schemes have been created for this purpose (such as stock options).

Necessary regulation

One might refer to these as “maneuvers” or “signals” because many of these transactions remain merely declaratory and are not actually carried out; others are carried out but are subsequently followed by a capital increase, thus having the opposite effect. This outcome therefore appears consistent with the hypothesis of price manipulation.

Conversely, when such transactions result in the cancellation of the repurchased shares and a corresponding reduction in both the cash reserves and the equity of the company in question, the company could find itself in difficulty should subsequent events (or opportunities) arise that require rapid and significant financing to address them; a situation which, incidentally, is consistent with a disciplined approach to shareholder-oriented governance, as the financial market is called upon to assess the situation.

As these few examples and initial observations show, it seems advisable for financial professionals, the general public, research institutions, and government authorities alike to recognize the challenges posed by this excessive reliance on share buybacks so that much-needed regulation can be put in place.

Elisabeth Walliser, Director of the IAE Nice, Research Group (GRM), Université Côte d’Azur and Roland Pérez, Professor Emeritus, Montpellier Research in Management, University of Montpellier

This article is republished from The Conversation under a Creative Commons license. Readthe original article.